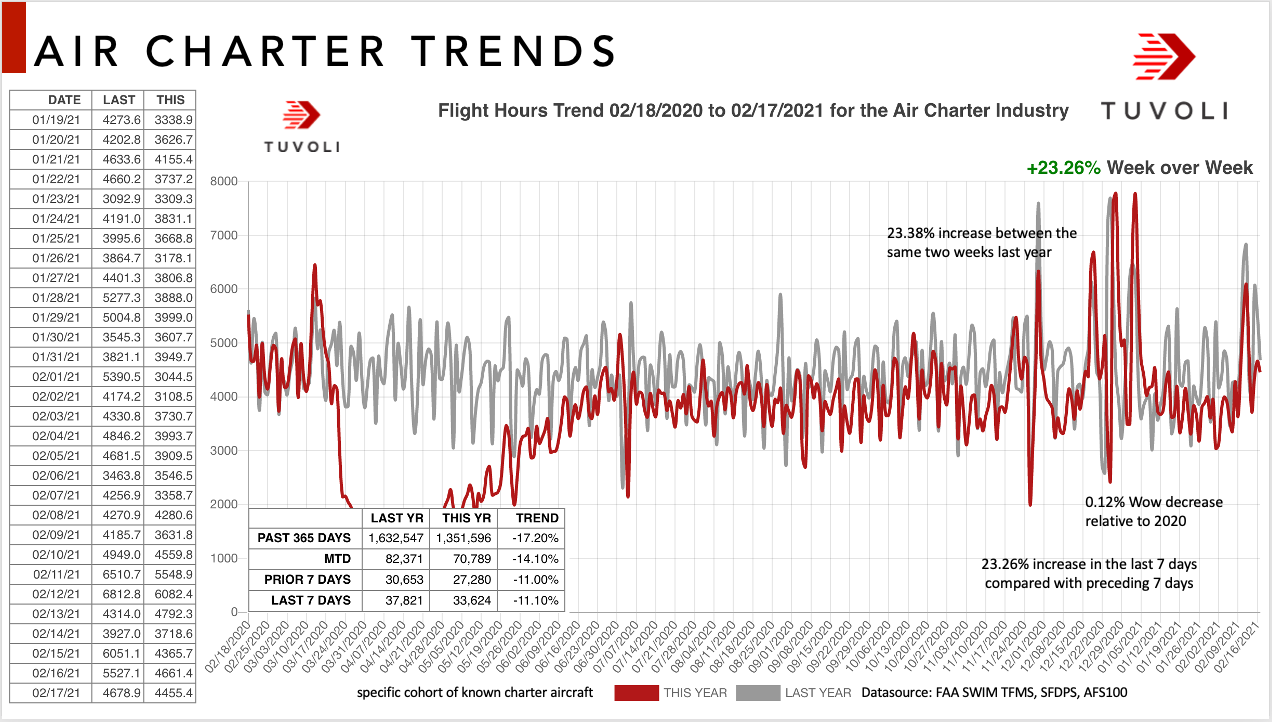

There was a healthy spike in volume over the past week due to President's Day weekend. As you'll see from the chart below the trend is up for the past two weeks relative to what we have seen as a trend... only down 11% where the trend has been 15-17%. The week-over-week increase for the President's day holiday was within 0.12% of the increase last year.

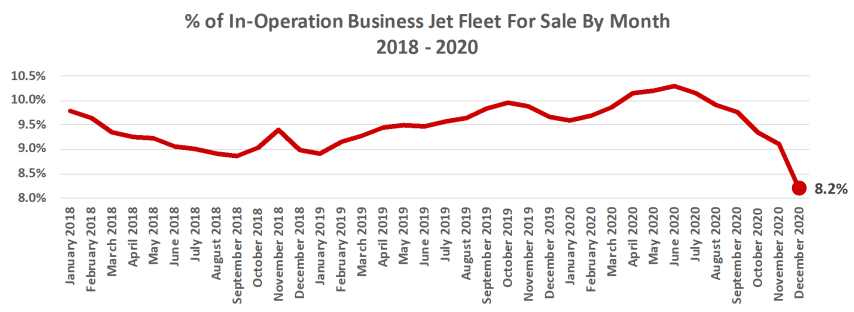

Early indications suggest that inventory has since shrunk even further, to just 1,776 jets on January 11, 2021 or just 7.9% of the fleet. Pre-owned pricing today is generally in alignment with expectations on both sides of the transactions table compared to May 2009 when for-sale jets peaked near 19% of the in-service fleet, the highest ever recorded. At 8% in January 2021, inventory as a percentage of the in-service fleet is now at its lowest recorded level to date in this millennium.

Although business jet flights were off YoY from -11% in Light up to -27% in Large most of the reduction in usage was in first half of 2020. Since then flights have recovered almost to normal with the exception of Large aircraft.

It is no surprise Large aircraft remain slow due to the continued pressures and difficulties with International Travel.

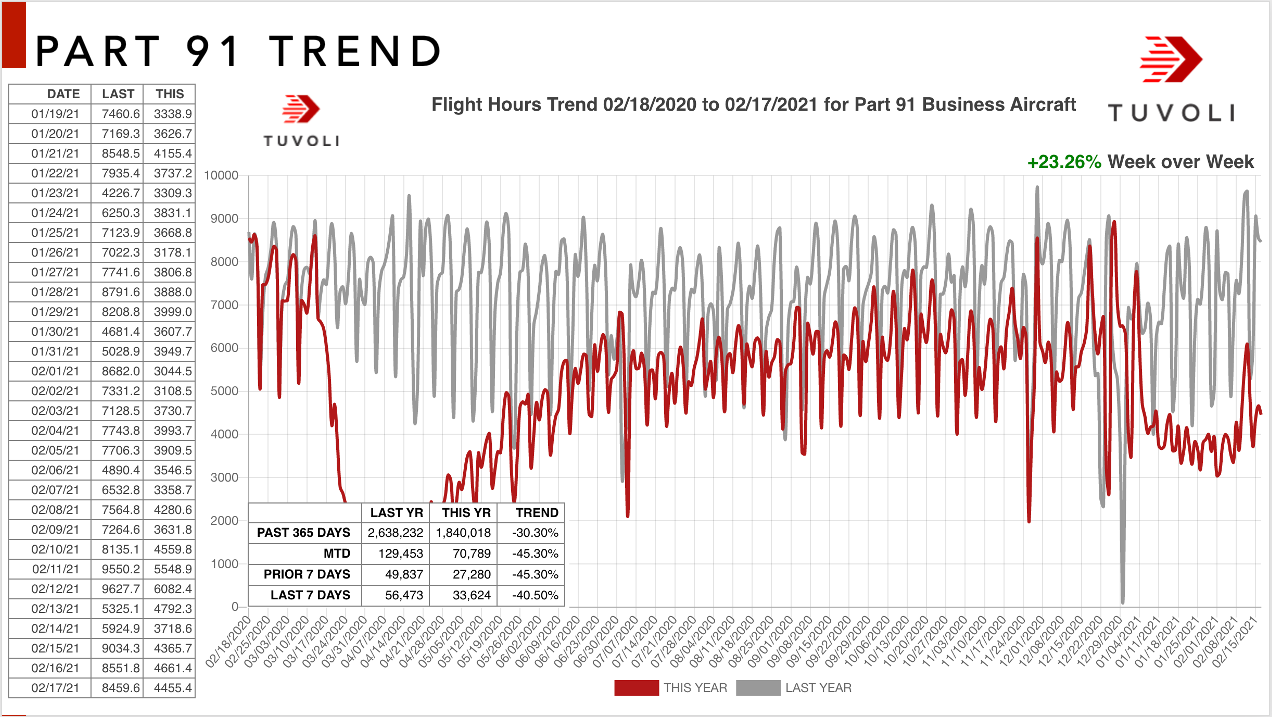

Charter P135 activity has mostly recovered to about 85% of pre-Covid-19 levels, but Business Private Part 91 flying remains stubbornly flat and down 30-40% from 2019 levels with the greatest decline in larger, longer range jets.

Much of this difference between Private Part 91 flying and Part 135 Charter could be attributed to new entrants into the private flying world that started chartering aircraft more or for the first time in 2020 due to Covid-19.

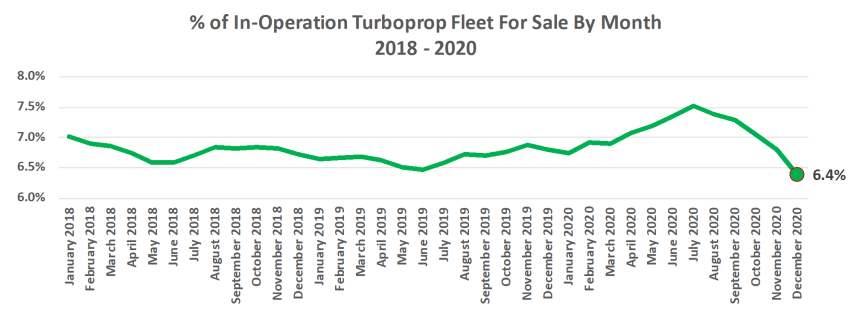

It is also becoming apparent that many Private flyers opted to purchase their own aircraft as well as represented in the declining available inventories numbers.

JETNET’s proprietary monitor of sentiment amongst aircraft owners / operators rebounded smartly in Q4 2020 across most regions of the world, based on JETNET iQ quarterly surveys.

Indicator at 58: Our Barclays Business Jet Indicator (BBJI) came in at 58, 18% higher from September and its highest level since late 2018, indicative of improving market conditions. Our straight up measure of overall business conditions came through at 5.9 (0-10 scale), 10% higher from September and reflective of a better than normal market.

COVID-19 impact: Over the short term, 56% of respondents expect higher demand (including 6% that expect much higher demand) on COVID-19 impact. Longer term, 71% of respondents (similar to our September survey) see higher demand on COVID-19 impact.

Election impact: Nearly half of respondents believe the Biden Administration will be negative for bizjet demand while 15% see it as positive, although nearly 40% see no impact at all.

Respondent commentary (pgs 13-14): Overall commentary reflects strong Q4 demand driven by heightened year-end tax activity post the election along with ongoing COVID-19 concerns that has driven an increasing number of first time buyers. Used market activity continues to be seen stronger as compared to new and small/midsize markets seen stronger as compared to large.

View on market: We forecast new delivery volumes rebounding slightly (<10%) to ~500 in 2021, albeit still ~30% lower from 2019, driven by improvement in small/mid while large lags.

Raising price target on TXT: Our revised $52 price target reflects a more positive view of the small/mid market and incorporates a blend of 9x EBITDA and 15x FCF/sh on our 2023 estimates, discounted back one year. Our prior $37 price target reflected a blend of 9x EBITDA and 8.0% through-cycle FCF yield (or 12x FCF/sh) on our 2022 estimates, discounted back a year.