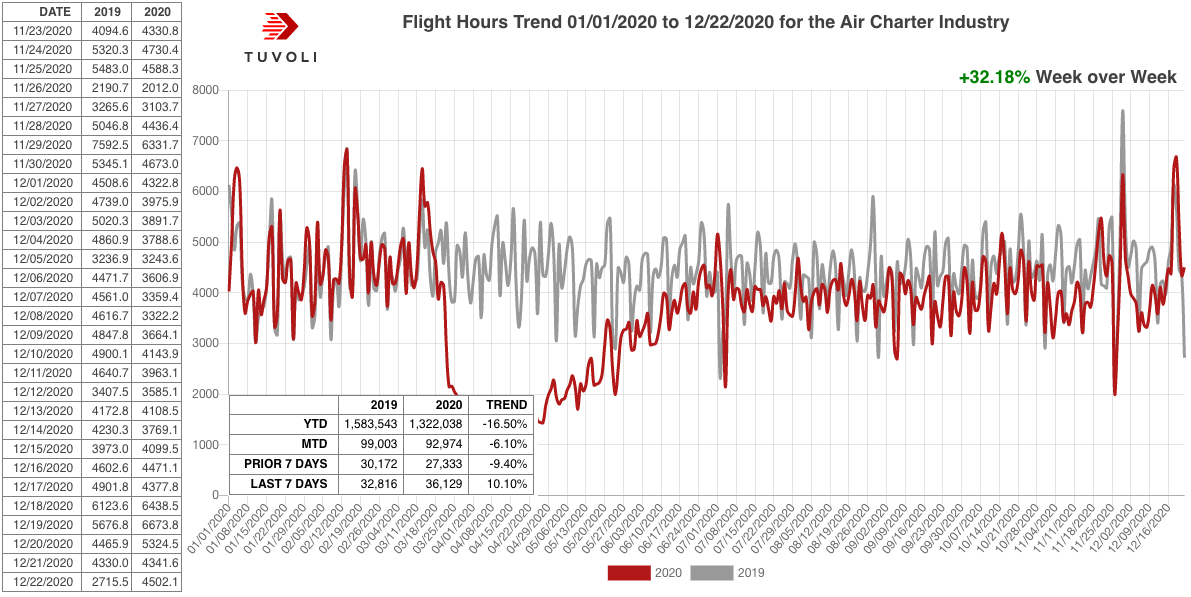

From all angles so far, Christmas demand has been historically strong. We have been above 2019 for the last five days. In similar fashion to Thanksgiving, the highest volume day so far has been the Saturday preceding the holiday, which follows the trend we have seen toward longer stays in general and in particular around holidays.

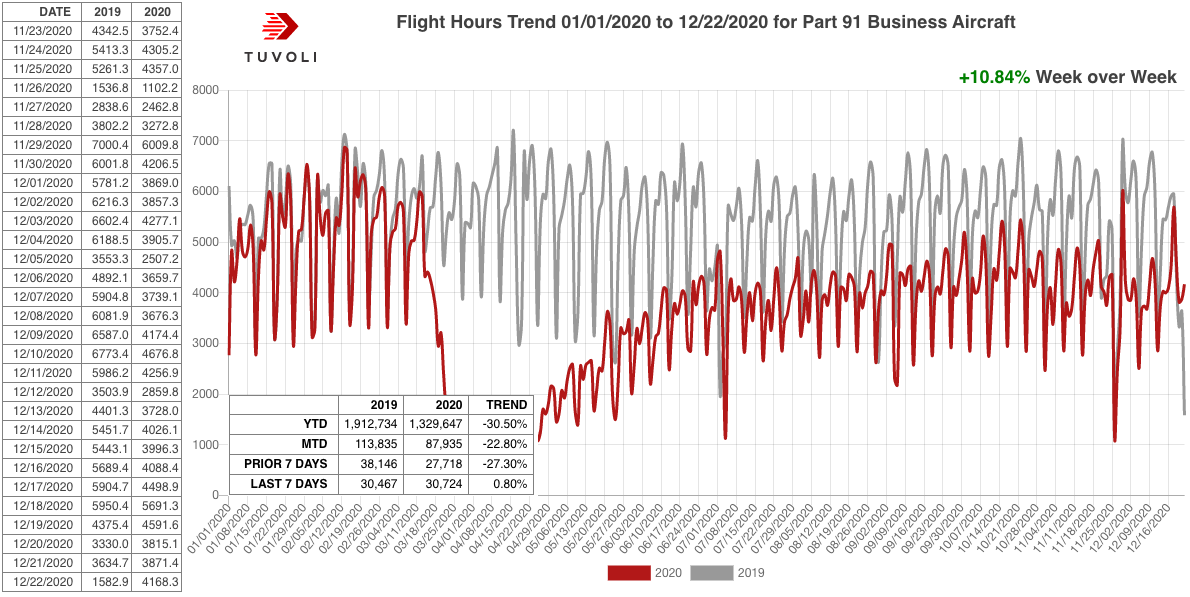

Remarkably, even Part 91 aircraft are trending above 2019 levels for the past week, showing volume levels we haven't seen since the pandemic began. For Part 91 operations, Friday was the peak day.

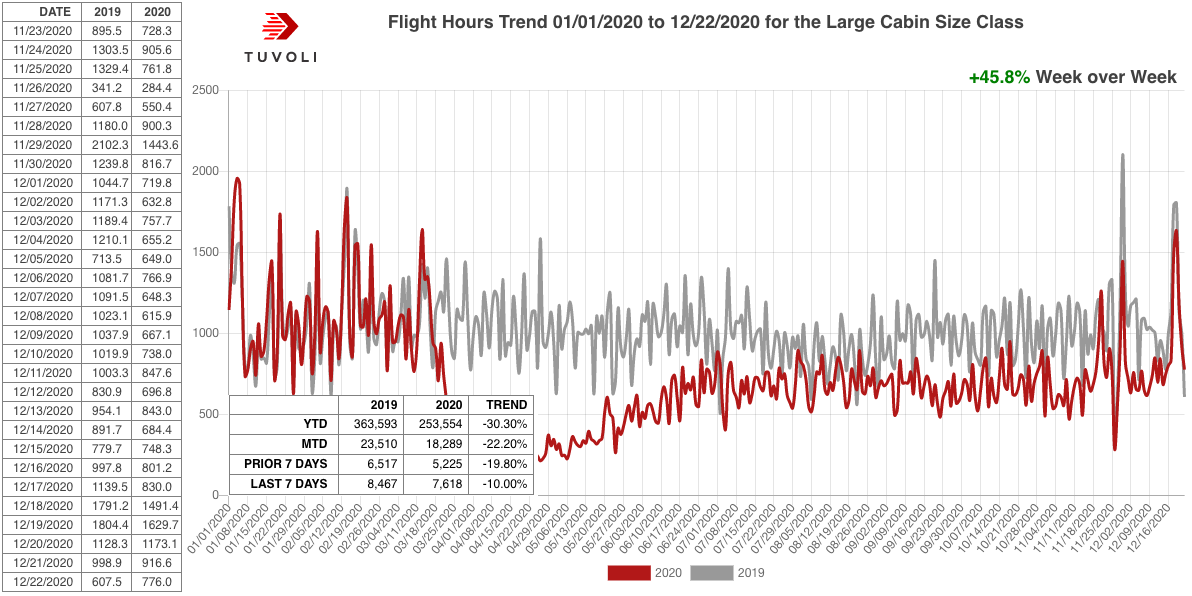

Large cabin aircraft are also showing the best numbers in a long-time.

When I looked at individual airports nearly all of them are showing YoY numbers above 2019. One exception is Aspen, which is trending below 2019 in light of their negative test/quarantine requirements. All-in-all, a strong end to a year that we will never forget.

No glut in available inventory—which had been hovering between 10.1 and 10.3 percent in pre-COVID months—occurred, either: 10.7 percent of the business jet fleet (2,264 aircraft) were for sale at August’s end. In contrast, in the wake of the 2008 market meltdown, inventory bloated from similar pre-crisis levels to some 18 percent of the fleet.

The passing decade has also brought acceptance that—irrational exuberance aside—preowned aircraft, like other capital equipment, declines in value. That lesson was made all the more brutal by the annual value declines of some 20 to 25 percent that many models endured in the immediate post-crash years. Though today’s value declines are greater than those in pre-crash times, the intervening shock made drops of recent years easier to plan for and bear.

WHY THE PREOWNED JET MARKET MIGHT BE STRONGER AFTER COVID

Meanwhile, a possible inventory shortage looms. Aircraft changing hands are getting older. The composite profile of a preowned business jet sold in the first half of 2019 was a 2004 model priced at $4.4 million; for the first half of this year, the aircraft was a 2002 vintage, sold for $3.7 million, according to JetNet. (The data service derived the figures from sales of the 236 business jet models it tracks.)

With a shortage of newer pedigrees, older airframes including early Citations, Hawker 700/800s, Bombardier Challengers, and Falcons and Gulfstreams into the vintage 900 and GIV series remain in demand, if they’ve been well maintained, refurbished, and upgraded, and are cosmetically appealing. Concurrently, lesser examples of these same models are being sold for the value of salvageable resale parts.

“A turnkey older business jet ready for operations will attract a substantial number of [cash] buyers,” says Jason Zilberbrand, president of aircraft valuation and appraisal service Vref.

Yet even as demand for late-model preowned aircraft grows, new business jet shipments will shrink about 22 to 25 percent this year, JetNet forecasts. A decline in new aircraft sales, of course, creates more squeeze in the preowned market.

“The largest segment of buyers for business jets in the U.S. is those looking for a sub-$5 million aircraft that can seat eight and travel over 2,500 nautical miles,” Zilberbrand says. “Until one of the manufacturers can build a midsize jet that doesn't breach the $15 million sales price, the preowned market will continue to attract buyers.”

Data from Argus shows Part 135 private jet charters continued to push the recovery of business aviation last month. In October, there were 802,054 flights, 8.7% below 2019 levels. That includes 14 days in which traffic was higher than the same date last year.

It marked an improvement from September when flights were down 12% year-over-year. During the steepest part of the COVID-19 crisis, Part 135 flights fell 67% in April, including a nadir on April 12 when they were off 84%.

Private Jet Flights by Month and Type (Year-over-year % change)

Month

Part 135

Part 91K

Part 91

March

– 26.8%

– 30.4%

– 35.4%

April

– 67.0%

– 80.4%

– 68.0%

May

– 47.01%

– 54.5%

– 45.9%

June

– 22.2.%

– 25.4%

– 27.8%

July

– 15.1%

– 19.2%

– 23.1%

August

– 16.5%

– 16.9%

– 24.9%

September

– 12.0%

– 12.2%

– 17.5%

October

– 8.7%

– 11.1%

– 16.9%

Argus data shows October Part 135 charter flights climbed within 10% of 2019 numbers on a year-over-year basis for the first time since the COVID-19 crisis.

Fractional share operators, likely powered by NetJets and Flexjet, which make up approximately 80% of the total, also had their best month since the outset of COVID, with 31,897 flights in October, down 11%. In September, Part 91K operators were off 12.1%. In April, flights were down 80.3%.

Part 91 flying continued to lag, although the year-over-year deficit improved to a 16.9% reduction in October compared to a 17.5% drop in September.

Global private jet outlook

Looking globally, WingX reports worldwide charter were down just 6% in October compared to 2019, while fractional operators saw activity down just 8%. However, it reports flights by private jets used exclusively by owners were off 20%.

Despite the many positive numbers, WingX managing director Richard Koe warns, “With the resurgence of the virus in Europe inevitably heading towards the United States, the industry faces a turbulent few months.”

He notes, “The business traveler isn’t going to come back in large numbers this winter so much depends on the sustainability of leisure demand, in particular for charter flights, with previously occasional customers flying more, and reportedly a significant number of first-time entrants coming into the market.”